February 2025 - Market Report

Tom Pantazis • February 15, 2025

As real estate professionals, we’ve always adapted to market cycles. But the challenge emerging in 2025 is different: it’s not cyclical—it’s structural. Climate change is no longer a distant concern for homeowners—it’s a present and growing risk with long-term implications, especially for retirees, fixed-income households, and those managing estates. Rising insurance premiums, unpredictable natural disasters, and localized value losses are changing how—and where—we buy, sell, and hold property. Whether you’re helping a family settle an estate or advising a senior client on a downsize, it’s critical to understand how these risks are starting to reshape the market. The Insurance Crisis Is the First Domino Property insurance—the backbone of financing and homeownership—is now at the center of the climate-risk conversation. In states like Florida and California, premiums are skyrocketing: Fort Myers, FL: Home insurance premiums have doubled in just two years (from $3,200 in 2022 to $6,300 in 2024). California: State Farm applied for a premium increase of up to 38%, citing the need to avoid financial instability and maintain ratings. These cost increases are not speculative—they’re directly impacting liquidity. Without affordable insurance, buyers can’t get financing. And without financing, sellers face price suppression or complete stagnation. Insight: If you or your clients are holding property in high-risk zones, be proactive. Get current insurance quotes before listing, and plan for longer days on market and possible buyer hesitation—even if the home itself is untouched by disaster. The Market Correction Has Already Begun In parts of Southwest Florida, where back-to-back hurricanes and high flood risk dominate, home prices are correcting sharply: Punta Gorda, FL: Home values dropped 35% year-over-year, per Redfin. Some streets have 5–6 homes for sale, and very little is moving. Why? Buyers are now calculating total cost of ownership, not just the list price. As insurance premiums climb and lenders scrutinize risk zones more carefully, the affordability picture changes—often drastically. David Burt, the financial strategist who warned of the 2008 housing collapse (and was portrayed in The Big Short), now calls this shift “The Great Repricing.” He estimates one in five U.S. homes may face 20–40% price drops over the next five years, not because of natural disasters themselves—but due to insurance availability and affordability. Insight: It’s time to assess your portfolio—or your clients’ portfolios—for geographic climate vulnerability. This includes homes in floodplains, wildfire-prone zones, and areas facing water scarcity. What It Means for Seniors, Executors, and Estate Planners For seniors living on a fixed income, and for estate executors managing the sale of inherited properties, this shift introduces real complications: Ongoing Insurance Costs: Seniors may be forced to sell not because of declining value, but because of rising monthly premiums. Estate Valuation Uncertainty: Market comparables are harder to trust in areas where value volatility is driven by external factors (like a pending insurance ruling or recent natural disaster). Liquidity Risk: Properties may sit longer on the market or sell for less than anticipated, particularly if buyers are struggling to secure affordable coverage. Insight: When advising on estate planning or probate liquidation, real estate now requires a climate-adjusted lens. Insurance, location-specific risk, and buyer financing capacity all factor into timeline, pricing, and return expectations. How to Advise Clients in 2025 and Beyond Here’s how to help clients—especially those with senior or estate-related needs—navigate the shifting climate and insurance landscape: 1. Run Insurance Quotes Early Before listing a home or recommending a purchase, get accurate insurance estimates. If a buyer can't finance the deal, no amount of marketing will sell the home. 2. Highlight Resilience Features Reinforced roofs, elevated foundations, and wildfire protection can be major selling points. These features not only reduce insurance costs—they also boost buyer confidence. 3. Know the Policy Landscape Stay informed on regional support programs. Florida and California are both introducing state-level subsidies to help homeowners retrofit and insure their properties. 4. Communicate Risk—and Opportunity Clients need context. A 35% value drop sounds terrifying—until you realize that homes purchased post-2020 boom were often significantly overvalued. Help clients interpret these numbers realistically. We are approaching a crossroads where climate risk and financial resilience will increasingly shape where—and how—we live. For estate executors, retirement-age sellers, and fixed-income homeowners, the pressure is already mounting in coastal and high-risk areas. This is not cause for panic—but it is cause for planning. As someone who specializes in estate and senior transitions, I help clients look beyond headlines and take informed, confident steps—whether that means repositioning an asset, listing a property, or reevaluating their homeownership strategy in a changing world. Let’s talk about your goals—and how to adjust for what’s ahead. Source: https://www.thetimes.com/business-money/companies/article/us-real-estates-next-crisis-is-climate-change-warns-big-short-guru-850p62jzh?utm

For years, the housing market has been defined by a dramatic shortage of available homes. But that era may be coming to an end. If current trends continue, the inventory crunch could be effectively resolved by spring 2026, with total unsold listings climbing back to “normal” levels we haven’t seen since before the pandemic. The big question is: what happens to home prices when that threshold is crossed? Let’s take a closer look at where inventory, pricing, and buyer behavior are headed—and what that means for your next real estate move. Inventory Is Climbing—Just Not Everywhere Available inventory of unsold single-family homes continues to build, rising to over 640,000 in late February—a 28.7% year-over-year increase. After three years of tight supply, this expansion is a pivotal shift. However, it’s not happening evenly across the country: California and Arizona now lead the way in inventory growth, with 45% more unsold homes than last year. Texas and Florida, which saw sharp inventory growth in 2023, are now more stable. The national trend points to an 18% increase in inventory by the end of 2025—a trajectory that would bring us back to 2018 levels of housing supply. Insight: The pace and geography of inventory growth will define local markets in 2025. For sellers in high-growth areas, pricing strategy is key. For buyers, more inventory means more choices—and more negotiating power. Home Prices: Rising, But Losing Momentum While home prices are still up about 2% year-over-year, the appreciation rate is slowing. That’s a clear signal that the balance between supply and demand is shifting. Here’s what we’re seeing: Median contract price in late February: $385,000 Price growth is half of what it was in 2024 (4%) 33.2% of homes on the market have had price cuts—more than any February in recent years This signals a compression effect: more listings mean sellers must appeal to a broader buyer base. Homes must be affordable to more people—not just the few who can still stretch their budgets in a high-rate environment. Insight: For those managing an estate or looking to downsize, this is a critical moment. The window to list and sell at strong prices remains open—but only if the property is priced and marketed effectively. Mortgage Rates Remain the Wild Card The 6% mortgage rate continues to be a psychological and financial tipping point for buyers. In late 2024, when rates briefly fell near 6%, demand picked up and home prices strengthened. As of February 2025, rates have eased slightly and remain below 2024 highs—but are still hovering near 7%. If rates drop below 6% for an extended period, we could see buyer demand rebound and inventory growth slow. If rates rise again, inventory may spike—and prices could soften. Insight: Your timeline should guide your decision more than interest rate forecasts. We help our clients plan around their needs, not wait for the market to make the decision for them. New Listings Remain Scarce Despite growing inventory, new listings are still below historic norms. Only 64,000 sellers listed homes in late February—a slight increase over 2024, but still modest. Many potential sellers remain on the sidelines, locked into ultra-low mortgage rates. This keeps supply growth gradual and prevents any kind of market “flood” from materializing. Even in areas like Washington, D.C., where unemployment is inching up, we’ve seen no significant increase in distressed listings. Insight: It’s important not to let fear or headlines dictate your strategy. We're monitoring these changes weekly, and as of now, there's no indication of a crash or wave of distressed properties. Will Prices Decline in 2025? That depends. With inventory likely to continue rising and mortgage rates still elevated, we could see flat or slightly negative price growth by year’s end—especially in rate-sensitive markets. Historically, when mortgage rates spike—like they did in 2022—prices dip temporarily. But when rates ease, demand returns quickly. We saw this in late 2024, and we could see it again in 2025. Insight: For sellers, the best way to protect value is by being ahead of the curve. Don’t wait for prices to peak—work with someone who understands your local market and can guide you through timing, presentation, and negotiation. Final Thoughts After years of imbalance, the housing market is beginning to normalize. Inventory is building. Price growth is slowing. And buyers are gaining leverage—especially if mortgage rates continue to decline. For my clients—whether you're preparing a probate listing, transitioning out of a long-held family home, or re-entering the market after time away—the key is clarity. Understand your options, know your local market, and align your next move with your life goals—not the headlines. If you’re wondering what 2025 means for your specific situation, let’s connect. We’ll look at the numbers, your needs, and create a plan that works. Sources: https://www.housingwire.com/articles/2025-could-be-the-last-year-of-inventory-shortage/ https://www.jpmorgan.com/insights/global-research/real-estate/us-housing-market-outlook

As we enter 2025, the conversation around affordability is louder than ever—and for good reason. Homeownership remains one of the most reliable paths to long-term wealth, but rising property taxes, insurance premiums, and interest rates have complicated that path for many buyers. Still, there are encouraging signs. Consumer confidence is growing, wage growth is improving, and new policies are beginning to reduce some financial barriers—especially for first-time buyers. Let’s break down what’s happening and what it means for buyers and sellers in today’s market. Homebuyer Confidence Is Rebounding Despite economic uncertainty at the end of 2024, housing sentiment has improved heading into February. According to recent surveys, 42% of buyers now believe mortgage rates will decline in 2025—up from just 31% the year prior. While only 22% say it’s a good time to buy, that number is rising from a historic low of 14% in late 2023. What’s fueling this optimism? Forecasted moderation of mortgage rates Slower home price appreciation Continued wage growth Insight: If you’ve been on the sidelines waiting for the “perfect” time, now may be the moment to refocus your strategy. Affordability remains a challenge, but market conditions are beginning to shift in the buyer’s favor. Rising Costs Are Still a Real Factor Affordability isn’t just about mortgage rates. In 2025, buyers are also dealing with: Property tax increases in fast-growing metros Rising insurance premiums, especially in climate-sensitive areas like Florida and parts of California Elevated home prices, which, while stabilizing, remain near record highs Even with rates stabilizing near 6.5% and some relief expected later this year, monthly housing costs remain high—especially for first-time homebuyers and seniors on fixed incomes. Tip for Buyers: Know your numbers. Understand not only your mortgage payment but also your estimated taxes, insurance, and maintenance. We help our clients map these out clearly so there are no surprises. Why Now Could Still Be the Right Time to Buy Spring often brings more listings—but it also brings more competition. Buying in February or March, before the market heats up, could offer key advantages: Less competition means fewer bidding wars and more negotiating power. Potential savings from winter price dips or seller incentives (especially on homes that sat through the holidays). More motivated sellers, who may be flexible on price or willing to cover closing costs. Insight: For those managing estate sales or considering a downsizing move, acting now—before spring listings flood the market—can position you ahead of the curve. Home Types Poised for Growth in 2025 Certain property types are expected to see value increases this year. If you’re buying or selling one of the following, you’re in a favorable position: Multifamily and ADU-equipped properties – Ideal for investors and multi-generational households Eco-friendly homes – Increasingly in demand among younger buyers Starter homes – Scarce and competitive, especially in entry-level markets Manufactured/modular homes – Gaining traction as affordable, customizable alternatives Seller Tip: Highlight what sets your property apart. Buyers are looking for value, flexibility, and potential income—especially in an affordability-focused market. Good News Ahead: Credit Score Relief May Be Coming In March 2025, a new rule from the Consumer Financial Protection Bureau (CFPB) is expected to remove unpaid medical debt from credit reports—potentially boosting credit scores by an average of 20 points. That’s good news for buyers who may have been just shy of qualifying for competitive mortgage terms. Estimated impact: 15 million Americans Expected benefit: Up to 22,000 additional mortgage approvals annually This shift could open the door to homeownership for many who have previously been sidelined. If you’re unsure how your credit history affects your buying power, let’s review it together. Affordability will continue to define the 2025 housing market—but that doesn’t mean opportunity is off the table. With inventory gradually improving and mortgage rates showing signs of moderation, buyers and sellers alike can benefit from being informed and prepared. If you’re navigating a transition—whether it’s settling an estate, helping a parent downsize, or preparing for your next chapter—I’m here to guide you through it. Together, we’ll build a plan that works in this market—not in theory, but in reality. Source: https://rwmloans.com/february-2025-changes-to-help-finances/

After a stretch of volatile mortgage rate hikes and shifting affordability, 2025 is ushering in a new phase for the housing market—one that favors preparedness over perfect timing. For clients navigating probate sales, legacy planning, or retirement transitions, understanding what’s really happening with rates and demand can help bring clarity and confidence to the decision-making process. Let’s take a look at the latest market dynamics and what they mean for your next step. Mortgage Rates Have Stabilized—But Don’t Expect Major Drops Mortgage rates began to ease toward the end of 2023 and dipped as low as 6.2% in September. However, by early 2025, they’ve rebounded to an average of 6.84%—with experts expecting them to hover around 6.5% for much of the year. The Mortgage Bankers Association, CoreLogic, and Freddie Mac all suggest the same thing: we’re entering a period of rate stability, not rapid decline. Affordability Challenges Continue—But the Market Is Rebalancing Affordability has been the market’s defining hurdle since 2022. Even with mortgage rates leveling out, inflation-driven costs, property tax hikes, and rising insurance premiums have kept the monthly cost of owning a home historically high. In January 2025: Median home price: $396,900 (a record for January) Average 30-year fixed mortgage: 6.84% Share of homes selling above asking: 22.4% Yet here’s what’s changing: inventory is growing. January marked the 15th straight month of rising listings, up 24.6% year-over-year. While still below pre-pandemic levels, this trend is a positive signal that supply is recovering. For sellers, more inventory means more competition—so pricing and preparation matter. For buyers, this is the time to get pre-approved and ready to act when the right opportunity arises. The Lock-In Effect Is Still Holding the Market Back One of the biggest forces still affecting market movement is the lock-in effect. Many homeowners refinanced into 2–3% mortgage rates during the pandemic. With today’s rates hovering around 6.5–7%, many are hesitant to sell and take on higher monthly payments. This has kept existing inventory tighter than it could be. However, builders are stepping in to fill the gap: 26% of builders reduced home prices in February 2025 59% offered incentives like mortgage rate buydowns New construction may offer better opportunities than resale for buyers looking to stretch their budget or avoid bidding wars—especially those downsizing or relocating after an estate transition. What About Home Prices? Growth Will Continue—but Slow Down After a record-high in June 2024, home prices are expected to keep rising—but at a more modest pace. CoreLogic forecasts just 2% growth for 2025 (down from 4.5% in 2024). In general: Markets with higher inventory (like Atlanta or Salt Lake City) may see minor price declines High-demand, low-supply metros (Miami, Boston, Denver) will continue to see appreciation If you’re looking to sell in 2025, market strength is still on your side. But overpricing a property in today’s climate can lead to extended days on market. Smart, data-driven pricing strategies will win. What This Means for Buyers and Sellers in 2025 For Buyers: You may not see much price relief—but you will see more options. Competition has cooled, builders are negotiating, and rates have come down from 2023 highs. If you’re debt-free, have a solid down payment, and are buying for the long term, this is a smart year to act. For Sellers (especially those managing estates or downsizing): Buyer demand remains solid, especially for well-maintained, move-in-ready homes. If your property is priced appropriately and presented well, you can still sell quickly and for strong value—even in a more competitive environment. Final Thoughts If we’ve learned anything from the last three years, it’s this: markets change fast. Waiting for the “perfect time” to buy or sell can lead to missed opportunities—especially for families navigating probate, retirees looking to simplify, or investors evaluating legacy assets. Instead of trying to time the market, focus on what you can control: Your financial readiness Your property’s value and positioning Your long-term goals Whether you’re preparing to list, buy, or just get clarity on your options, I’m here to help you move forward with confidence, not hesitation. Let’s talk strategy. Sources: https://www.ramseysolutions.com/real-estate/housing-market-forecast?srsltid=AfmBOopHTElr3vy-zi-8gzEfFZqCworsJ8it_AcdkdDW3JZer3HgxIOo&utm https://www.bankrate.com/real-estate/housing-market-2025/?utm

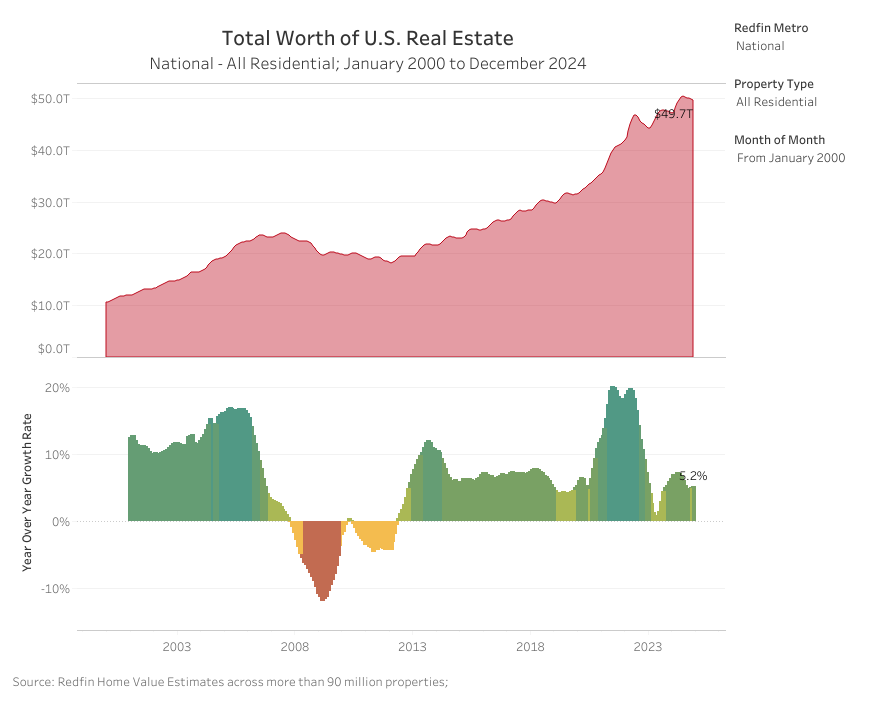

As 2024 comes to a close, we can confidently say this year reshaped more than just property values—it redefined how we think about homeownership, affordability, and long-term real estate strategy. What began with hopeful predictions for declining rates quickly became a year of volatility, innovation, and hard-earned resilience. For those of us serving clients navigating probate sales, retirement transitions, or generational wealth planning, 2024 offered both challenges and opportunities. Here’s a look back at the key forces that shaped the market—and what they might mean as we prepare for 2025. 1. Interest Rates Remained a Moving Target At the start of the year, the consensus was that mortgage rates would slowly decline, easing pressure on buyers and improving overall affordability. That didn’t happen. Rates surged in the spring, sidelining many would-be buyers and putting downward pressure on transaction volume. Even with a brief rate cut in September and another in November, mortgage rates remained elevated, hovering near 7% for much of the year. The volatility made planning difficult for both buyers and sellers, and the uncertainty filtered through every corner of the market. As Selma Hepp, Chief Economist at Cotality, noted, the bond market’s reaction to inflation concerns and federal deficit spending kept rates stubbornly high. While we saw brief moments of increased refinancing and pending sales, momentum was short-lived. What this means for 2025: A stable rate environment may not arrive until the second half of the year. Clients considering estate sales or major moves should be prepared to act decisively when rates dip, but not rely on timing the market perfectly. 2. Affordability Hit a Wall 2024 marked a new affordability ceiling. The cost of owning a home—when adjusted for inflation and income—reached its highest level in decades. And it wasn’t just about rising home prices or higher interest rates. Increased property taxes, rising insurance premiums, and inflation-related expenses have made homeownership more expensive across the board. For many of our clients—especially seniors on fixed incomes or families managing inherited property—this created a significant planning challenge. Key stat: Monthly mortgage payments today rival those during the Great Financial Crisis. Yet, because of slower wage growth, housing consumes a greater share of household income than ever before. 3. Inventory Shortages Persisted—But Showed Signs of Shifting The so-called “lock-in effect” kept many homeowners from selling. With ultra-low rates secured during previous refinancing booms, homeowners were reluctant to trade a 3% mortgage for a 7% one. But change is beginning. Life transitions—divorce, downsizing, estate settlement—brought more homes to market. In tight markets like California, we saw an uptick in new listings. In states like Texas and Florida, where construction boomed in recent years, inventory expanded more meaningfully. Takeaway: While inventory remains constrained, the logjam is beginning to loosen. This is particularly relevant for those exploring probate sales—timing and local market insights will matter more than ever in 2025. 4. Buyers Got Creative: The Rise of House Hacking and Shared Equity With traditional paths to homeownership increasingly out of reach, younger buyers turned to alternative solutions. Shared equity models, house hacking, and multi-generational buying grew in popularity. This shift wasn’t just about affordability—it was about flexibility and resourcefulness. And it wasn’t just buyers adapting; forward-thinking developers began offering duplexes and small multifamily units in response. For professionals: Expect continued demand for flexible housing options. Sellers with properties offering rental income potential may find strong interest, especially from millennial and Gen Z buyers. 5. The Market Grew in Value—But Slower Than Years Past Despite affordability concerns, the total U.S. housing market still grew by $2.5 trillion in 2024, bringing the combined value to $49.7 trillion. That’s a 5.2% year-over-year increase—modest by recent standards, but significant nonetheless. Much of this growth came from increased values in upstate New York metros like Albany and Rochester. Meanwhile, Florida—once red-hot—slowed due to climate risk, insurance hikes, and overbuilding. Notable trends this 2024: Millennials now own over 20% of the housing market, with a total value of $9.7 trillion. Rural home values grew 6.4%, outpacing urban and suburban markets for the seventh consecutive year. The number of homes worth $1 trillion or more continues to grow, with San Diego and Seattle poised to join that list in 2025. Final Thoughts 2024 wasn’t the easiest year to navigate—but it was a year of learning, growth, and strategy. For those managing estate assets, transitioning into retirement, or supporting family members through life’s changes, the real estate market continues to be a powerful tool when used with intention. My message to clients and fellow professionals alike is this: Be ready. 2025 won’t eliminate the challenges we’ve seen, but it will open doors for those who are prepared. Rates will fluctuate. Inventory will shift. And timing will matter. Whether you’re holding onto property with generational value, considering a strategic sale, or planning for the next phase of homeownership, I’m here to offer clarity, consistency, and trusted guidance—every step of the way. Let’s move forward with purpose. Sources: https://www.cotality.com/insights/articles/2024-look-back-housing-market-trends https://www.redfin.com/news/housing-market-value-december-2024/